Companies importing goods into the United States typically must collect customs duties (tariffs). The government collects tens of billions of dollars in duties each year. These numbers are only set to grow as tariff rates continue to rise.

But like the federal tax system, the customs system relies largely on private actors (here, importers and their partners) to accurately report relevant information (e.g., the type of good imported, its value, and its country of origin) and make appropriate payments to the government.

Increasingly, the government relies on whistleblowers to expose customs fraud. And through the False Claims Act, the federal government’s premier whistleblower law, individuals with knowledge of customs fraud can tip off the government and, if their case proves successful, obtain awards up to 30% of the recovery in return for their information.

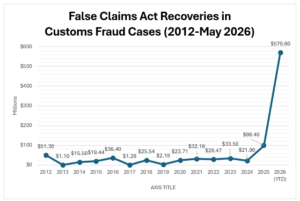

To date, the FCA has fueled over $968 million in customs fraud recoveries. 93% of successful customs fraud FCA cases have been filed by whistleblowers.

What are Custom Duties?

Custom duties are taxes on imported goods which are levied primarily to protect American businesses from unfair foreign competition. Duties are based on a percentage of the value of the imported goods. The Harmonized Tariff Schedule (HTS) sets out duties on countless goods. The U.S. Department of Commerce sets these tariff rates.

The highest duties are often focused on curtailing two forms of predatory competition: dumping and unfair foreign subsidies – however, tariffs may serve other goals too. These duties are Anti-Dumping and Countervailing Duties (AD/CVD). Because AD/CVD duties are so high, the incentive to evade them is particularly acute. Many of the largest customs fraud recoveries in history have involved AD/CVD duties.

Anti-Dumping Duties: Anti-dumping duties are meant to curtail, as the name implies, “dumping.” Dumping occurs when a company exports a product and sells it at an unduly low price—generally below the price it sells the product in its home market or even below the cost of production.

Anti-Dumping Duties: Anti-dumping duties are meant to curtail, as the name implies, “dumping.” Dumping occurs when a company exports a product and sells it at an unduly low price—generally below the price it sells the product in its home market or even below the cost of production.

Countervailing Duties. Countervailing duties are aimed at countering unfair foreign government subsidies of goods. Those subsidies can give foreign companies an unfair leg up in the American marketplace.

Countervailing Duties. Countervailing duties are aimed at countering unfair foreign government subsidies of goods. Those subsidies can give foreign companies an unfair leg up in the American marketplace.

How Are Customs Duties Enforced?

United States Customs and Border Protection (CBP) collects duties and principally enforces the operative tariff laws. However, the Department of Justice (DOJ) may also be involved.

What is Customs Fraud?

Customs fraud is the fraudulent practice of reducing or wholly evading custom duties on imported goods. The government largely relies on importers to ensure that appropriate duties are collected. That fact, coupled with the sheer amount of goods imported into the United States, creates an opportunity for illegal conduct. After all, the government can only inspect a tiny percentage of shipments on entry.

Customs fraud creates two key public policy problems:

First, it cheats the government out of money which it is legally owed. And when the government loses revenue, every taxpayer bears the cost.

Second, companies engaged in customs fraud are able to improperly sell goods at unfairly low prices—thus undercutting companies that play by the rules. This creates an uneven competitive playing field.

What are Examples of Customs Fraud?

Customs fraud comes in many flavors but among the most common schemes are the following:

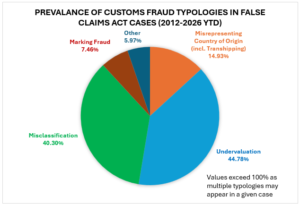

Misclassification: Companies mislabel goods under inappropriate HTS codes in order to avail themselves of lower tariff rates. In some cases, the subterfuge is more sophisticated than merely attaching the wrong HTS code to the goods. For example, the importer and exporter may work together to physically disguise the goods to make them appear as if they are another product.

Misclassification: Companies mislabel goods under inappropriate HTS codes in order to avail themselves of lower tariff rates. In some cases, the subterfuge is more sophisticated than merely attaching the wrong HTS code to the goods. For example, the importer and exporter may work together to physically disguise the goods to make them appear as if they are another product.

Undervaluation: Given that duties are tied to the value of the imported goods, another simple and common way to engage in customs evasion is by claiming that the product is worth less than it really is.

Undervaluation: Given that duties are tied to the value of the imported goods, another simple and common way to engage in customs evasion is by claiming that the product is worth less than it really is.

This often occurs via “double invoicing” where an exporter issues a lower (fraudulent) invoice to the importer and a higher invoice that reflects the actual payment. In some cases, an importer may split its payments into two different transactions and only declare the value of just one transaction to customs. This provides further obfuscation of the illegal arrangement because, if probed by CBP, the importer can at least point to a real bank transaction to back up the dubious invoice.

There are other forms of undervaluation, however. For example, related parties may set transactions at a below arm’s length price or improperly apply the “first sale rule” which applies, under strict conditions, to certain overseas transactions where the goods are destined for U.S. Soil.

Country of Origin Falsification and Transshipping: Custom duties are levied based on the country of origin. Customs evaders may declare a false country of origin upon entry. In many cases, the importer may ship goods through one or more intermediary countries which have lower (or no) tariff rates than the country of origin, in order to falsely declare the intermediary country as the country of origin. For example, a fraudster may ship goods from China (which is subject to high tariffs) to Canada (which is subject to much lower tariffs) and declare that the goods are Canadian upon entry in the United States.

Country of Origin Falsification and Transshipping: Custom duties are levied based on the country of origin. Customs evaders may declare a false country of origin upon entry. In many cases, the importer may ship goods through one or more intermediary countries which have lower (or no) tariff rates than the country of origin, in order to falsely declare the intermediary country as the country of origin. For example, a fraudster may ship goods from China (which is subject to high tariffs) to Canada (which is subject to much lower tariffs) and declare that the goods are Canadian upon entry in the United States.

Assist Fraud: Domestic companies often provide “assists” to foreign manufacturers. An “assist” covers a range of items and services provided by domestic companies to their foreign trade partners (from tools and dies to components and design work) that facilitate the production of goods. When assists are provided, they must be accounted for in the value of goods upon entry. In order to reduce the valuation of their goods, companies often exclude assists from the declared valuation.

Assist Fraud: Domestic companies often provide “assists” to foreign manufacturers. An “assist” covers a range of items and services provided by domestic companies to their foreign trade partners (from tools and dies to components and design work) that facilitate the production of goods. When assists are provided, they must be accounted for in the value of goods upon entry. In order to reduce the valuation of their goods, companies often exclude assists from the declared valuation.

Marking Fraud: Imported goods must physically reflect their country of origin with a “marking.” Goods that lack this marking are assessed additional duties as a penalty. Companies—particularly those involved in country of origin fraud—often avoid marking their goods or mark them with a false country of origin.

Marking Fraud: Imported goods must physically reflect their country of origin with a “marking.” Goods that lack this marking are assessed additional duties as a penalty. Companies—particularly those involved in country of origin fraud—often avoid marking their goods or mark them with a false country of origin.

Structuring: Structuring occurs when a large shipment is split up so as to make it appear that numerous, smaller claimed shipments occurred. By splitting up a large shipment into smaller ones, importers can then claim the “de minimis” exemption which allows importers to avoid duties entirely for certain small transactions. While the de minimis exemption has now been withdrawn, the statute of limitations on these claims may not have expired depending on the facts of the case.

Structuring: Structuring occurs when a large shipment is split up so as to make it appear that numerous, smaller claimed shipments occurred. By splitting up a large shipment into smaller ones, importers can then claim the “de minimis” exemption which allows importers to avoid duties entirely for certain small transactions. While the de minimis exemption has now been withdrawn, the statute of limitations on these claims may not have expired depending on the facts of the case.

What are Hot Areas for Customs Enforcement?

The federal government targets all forms of customs evasion in all industries. However, certain hot spots arise.

Chinese Goods: Around 80% of FCA customs fraud cases have involved Chinese goods which is to be expected given that China is a major trade partner and subjected to very high duties.

AD/CVD: AD/CVD duties are often prohibitively high (and that is by design). That means that those involved in importing goods subject to AD/CVD have a greater incentive to skirt the law. It also means that damages in these cases can be very substantial. And because AD/CVD duties are often aimed at protecting critical domestic industries, DOJ is especially interested in pursuing those that evade these critical tariffs.

Low-Margin Goods: Those involved in the importation of low-margin goods may engage in customs fraud because they can ill afford to pay duties which cut into their already thin margins. While both low- and high-margin goods can be targets for enforcement, the temptation to defraud is especially high in the world of commoditized goods.

How Does the FCA Whistleblower Law Work?

The False Claims Act, the federal government’s oldest and most successful whistleblower statute, covers a wide array of frauds on the government, including customs fraud. This is because the False Claims Act addresses not just affirmative frauds on the government (e.g., illegally obtaining money from the government) but also cases where actors illegally evade their obligation to pay money owed to the government (e.g., customs fraud).

Among other remedies, the False Claims Act provides for treble (triple damages) and whistleblower awards for up to 30% of the government’s recovery.

The United States Department of Justice, which investigates and litigates FCA cases, has shown a growing interest in pursuing whistleblower cases involving customs fraud. Whistleblowers are critical for enforcement because customs fraud is particularly difficult to root out. While CBP provides some degree of oversight, it can only inspect and actively police a very small number of shipments. Whistleblowers with knowledge of customs fraud can prove to be invaluable partners to the government.

How Much has the Government Recovered in Customs Fraud Cases under the FCA?

The government has recovered over $968 million in customs fraud cases. Over half of that has come in 2026 alone, reflecting the remarkable growth of the FCA as a customs fraud enforcement tool.

How Much Do Whistleblowers Receive in Successful Customs Evasion Cases?

Under the FCA, a successful whistleblower (called a “relator”) is generally due between 15% and 30% of the recovery. Defendants can also be ordered to pay the whistleblower’s attorney’s fees. While awards are fact dependent, because federal recoveries can be very large, awards can be sizable. For example, a whistleblower in a recent customs evasion case concerning the misclassification of aluminum extrusions was awarded over $96 million. In another case, a customs fraud whistleblower was awarded $9.75 million.

Who Can Be a Customs Fraud Whistleblower?

Whistleblower eligibility is broad. With few exceptions, just about anyone can be a relator. The most common whistleblowers are current or former employees of companies involved in customs fraud. Increasingly, competitors—who have critical insight into their rival’s import practices and who have an economic interest in ensuring an even playing field—are filing cases. Customs brokers and others that have insight into the supply chain can also serve as whistleblowers.

Exemplary False Claims Act Recoveries Arising from Allegations of Customs Fraud

Recent years have shown a surge in FCA recoveries involving customs fraud. Many of these cases have involved goods imported from China. With the recent increases in duties on Chinese goods under the Trump administration, there will surely be more fraud involving the importation of Chinese goods for years to come.

- Perfectus Aluminum ($549.5 million): In May 2026, DOJ announced a $549.5 million settlement in a case involving alleged misclassification of aluminum extrusions. Defendants were accused of spot welding Chinese aluminum extrusions (which are subject to very high AD/CVD) to make them appear as if they were aluminum pallets because such pallets were subject to lower duties. One of the whistleblowers in this case was a rival aluminum firm.

- Ceratizit ($54.4 million): In December 2025, DOJ announced a $54.4 million recovery in a case involving the importation of Chinese tungsten carbide. The importer was accused of engaging in a multifaceted fraud scheme that involved transshipment through Taiwan, misclassification, and marking fraud.

- Farjess and Royal Canadian Steel ($19 million): Two companies and an individual defendant agreed to pay $19 million to resolve allegations that they lied about the country of origin of flat-rolled steel. The whistleblower was a customs broker who had worked with one of the defendant companies.

- International Vitamins Corporation ($22.8 million): A vitamin and supplement company agreed to pay $22.8 million in a case involving allegations that it had used the wrong HTS codes for dozens of imported products.

How Can I Blow the Whistle on Customs/Tariff Fraud?

Filing a False Claims Act case allows whistleblower to inform the government of customs fraud while providing the opportunity to seek a whistleblower award. The False Claims Act also provides certain anti-retaliation protections.

An experienced whistleblower attorney can explain the risks and rewards associated with pursuing a case. Our firm, Pietragallo Gordon Alfano Bosick & Raspanti, LLP, has represented whistleblowers for decades and has a wealth of experience in partnering with the government. We are among the country’s premier whistleblower firms and we know the customs laws, supply chain industry, and the FCA well.

Contact us if you are interested in pursuing a customs fraud whistleblower case. An initial consultation is free and confidential.